Homebuying Process Tips: Getting Approved for VA Loan

One standout benefit of serving in the military, National Guard, or Reserves is your qualification to apply for a VA mortgage. Administered through a broad range of lending institutions, VA loans are guaranteed by the federal government. That’s why they usually feature lower interest rates and more flexible qualification standards. Many service members buy their homes through the VA with no money down. Overall, lenders consider VA loans less risky than conventional private mortgages.

To be eligible for a VA loan, you need to be an active or former member of the military. In general, you must have been honorably discharged, although there are rare exceptions to that rule. Additionally, surviving spouses of veterans can also apply for a VA loan unless they have been remarried. Depending on when you served and why you were discharged, there are service benchmarks you must meet in terms of time served. But to be clear just because you qualify to apply for a VA mortgage, doesn’t necessarily mean you’ll be able to secure one. Here are several tips for increasing your chances of being approved to take advantage of this useful benefit.

Don’t Let the Paperwork Get to You

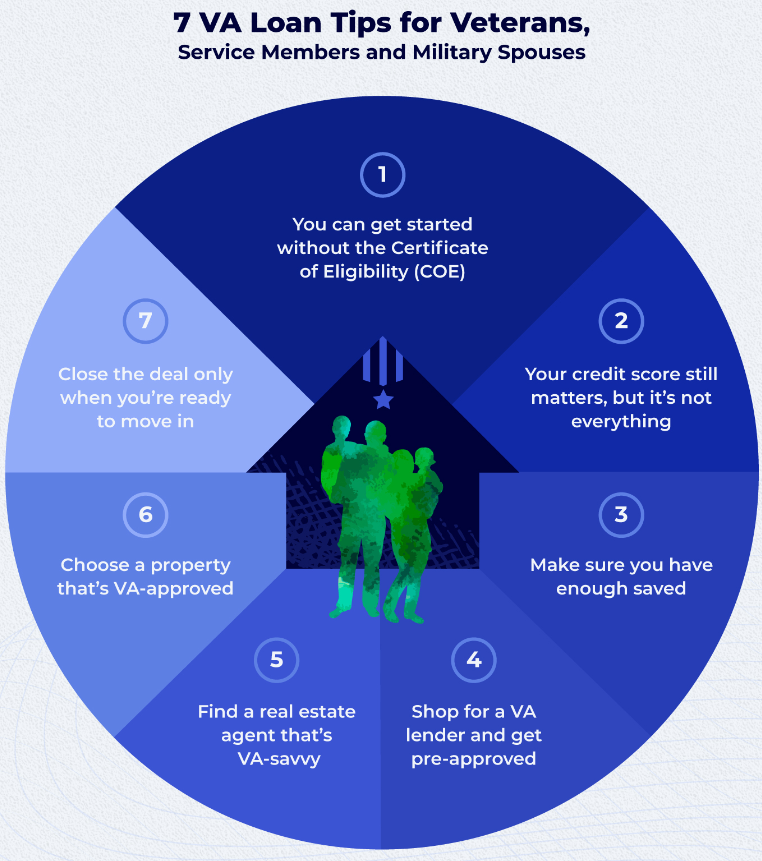

Applying for any mortgage can be confusing and time-consuming. But VA loans come with an additional layer of complexity. Anything involving the government comes with red tape, right? First, you’ll need to secure a Certificate of Eligibility to be approved for a VA loan, which involves gathering a little more documentation than you would need to apply for a conventional loan. But you don’t need to have a certificate to begin the VA loan application process. In fact, most lenders will be glad to assist you in getting one. Remember that lenders want your business. And a good one will bend over backwards to get it.

Your New Home Must Be Eligible, Too

Here’s why working with a VA loan-savvy realtor can be a tremendous boon. The last thing you want to do is spend lots of time trying to purchase a property that won’t qualify for a mortgage in the end. The government doesn’t want to invest in properties that have major defects and neither do you. They’ve established a set of Minimum Property Requirements for homes purchased under the VA loan program. Your realtor or lender can explain these to you and help you steer clear of properties that don’t stack up to VA standards.

Get Familiar with Acceptable Use and Occupancy Guidelines

VA loans aren’t made for every type of property. Loans are only written for primary residences. Your new home can be a Colonial, a condo, a manufactured home, or anywhere in between but you have to live there. You can even take out a loan to build a home from scratch. But vacation homes and investment properties aren’t eligible for VA financing. In addition, the VA sets time limits around occupancy. Generally, you must move into your home within 60 days of closing. If you’re currently deployed, that rule can be challenging. A spouse can substitute for a deployed service member to meet the occupancy date, but single people may have a harder time fulfilling the requirement. It can be done, though.

Your Credit Does Counts

One important advantage VA loans have over traditional mortgages is that VA borrowers are subject to more lenient financial qualifications. Officially, there is no credit score bar you have to clear before you can be approved for a VA mortgage. But having good-to-excellent credit can help you secure a larger loan and/or a better interest rate.

Even a quarter-point difference in the interest rate you’re offered can amount to thousands of dollars over the life of your mortgage. That’s why getting your credit in the best possible shape before you apply for a loan is essential. Download a free copy of your credit report from each of the three credit reporting bureaus to see where you stand. Then do whatever credit repair that needs to be done. Make sure all of your credit accounts are current—and stay that way—while you’re applying for a mortgage. Close any accounts that you’re no longer using. If you find any negative remarks on your report that aren’t legitimate, dispute them. Fixing mistakes on your credit report can take some time. So be sure you attend to your credit well in advance of submitting a loan application.

Remember to Get Pre-Qualified Before You Start House Hunting

Today’s real estate market is very competitive. Nowadays, home sellers are inundated with offers and 43% accept one within a week of listing their homes. Sellers aren’t interested in wasting time and want to talk to serious buyers only. Prequalifying for a loan through one or more lenders—that is, securing a letter that states how much money a lender would be likely to loan you and at what interest rate—is one way to show home sellers that it’s worth their time to work with you. Many home sellers won’t even entertain offers from buyers who aren’t prequalified.

Getting prequalified also can help you set home price parameters for yourself and hone in on properties you can reasonably afford. It’s easy to do. And it won’t affect your credit score, even if you prequalify with more than one lender. As someone who has served our country, you’re entitled to the rewards a VA mortgage can provide. And you’re entitled to great service from the professionals you work with during the home buying process.

7-va-loan-tips.jpg

One standout benefit of serving in the military, National Guard, or Reserves is your qualification to apply for a VA mortgage. Administered through a broad range of lending institutions, VA loans are guaranteed by the federal government. That’s why they usually feature lower interest rates and more flexible qualification standards. Many service members buy their homes through the VA with no money down. Overall, lenders consider VA loans less risky than conventional private mortgages.

{kind=link}

To be eligible for a VA loan, you need to be an active or former member of the military. In general, you must have been honorably discharged, although there are rare exceptions to that rule. Additionally, surviving spouses of veterans can also apply for a VA loan unless they have been remarried. Depending on when you served and why you were discharged, there are service benchmarks you must meet in terms of time served. But to be clear just because you qualify to apply for a VA mortgage, doesn’t necessarily mean you’ll be able to secure one. Here are several tips for increasing your chances of being approved to take advantage of this useful benefit.

Don’t Let the Paperwork Get to You

Applying for any mortgage can be confusing and time-consuming. But VA loans come with an additional layer of complexity. Anything involving the government comes with red tape, right? First, you’ll need to secure a Certificate of Eligibility to be approved for a VA loan, which involves gathering a little more documentation than you would need to apply for a conventional loan. But you don’t need to have a certificate to begin the VA loan application process. In fact, most lenders will be glad to assist you in getting one. Remember that lenders want your business. And a good one will bend over backwards to get it.

Your New Home Must Be Eligible, Too

Here’s why working with a VA loan-savvy realtor can be a tremendous boon. The last thing you want to do is spend lots of time trying to purchase a property that won’t qualify for a mortgage in the end. The government doesn’t want to invest in properties that have major defects and neither do you. They’ve established a set of Minimum Property Requirements for homes purchased under the VA loan program. Your realtor or lender can explain these to you and help you steer clear of properties that don’t stack up to VA standards.

Get Familiar with Acceptable Use and Occupancy Guidelines

VA loans aren’t made for every type of property. Loans are only written for primary residences. Your new home can be a Colonial, a condo, a manufactured home, or anywhere in between but you have to live there. You can even take out a loan to build a home from scratch. But vacation homes and investment properties aren’t eligible for VA financing. In addition, the VA sets time limits around occupancy. Generally, you must move into your home within 60 days of closing. If you’re currently deployed, that rule can be challenging. A spouse can substitute for a deployed service member to meet the occupancy date, but single people may have a harder time fulfilling the requirement. It can be done, though.

Your Credit Does Counts

One important advantage VA loans have over traditional mortgages is that VA borrowers are subject to more lenient financial qualifications. Officially, there is no credit score bar you have to clear before you can be approved for a VA mortgage. But having good-to-excellent credit can help you secure a larger loan and/or a better interest rate.

Even a quarter-point difference in the interest rate you’re offered can amount to thousands of dollars over the life of your mortgage. That’s why getting your credit in the best possible shape before you apply for a loan is essential. Download a free copy of your credit report from each of the three credit reporting bureaus to see where you stand. Then do whatever credit repair that needs to be done. Make sure all of your credit accounts are current—and stay that way—while you’re applying for a mortgage. Close any accounts that you’re no longer using. If you find any negative remarks on your report that aren’t legitimate, dispute them. Fixing mistakes on your credit report can take some time. So be sure you attend to your credit well in advance of submitting a loan application.

Remember to Get Pre-Qualified Before You Start House Hunting

Today’s real estate market is very competitive. Nowadays, home sellers are inundated with offers and 43% accept one within a week of listing their homes. Sellers aren’t interested in wasting time and want to talk to serious buyers only. Prequalifying for a loan through one or more lenders—that is, securing a letter that states how much money a lender would be likely to loan you and at what interest rate—is one way to show home sellers that it’s worth their time to work with you. Many home sellers won’t even entertain offers from buyers who aren’t prequalified.

Getting prequalified also can help you set home price parameters for yourself and hone in on properties you can reasonably afford. It’s easy to do. And it won’t affect your credit score, even if you prequalify with more than one lender. As someone who has served our country, you’re entitled to the rewards a VA mortgage can provide. And you’re entitled to great service from the professionals you work with during the home buying process.